[ad_1]

I used to consider, as others do, that the “correct” Advance-Decline (A-D) information come from the “frequent” shares. In any case, they’re the actual shares, so they need to know higher what the inventory market is doing. I finished believing that after I appeared on the information.

Among the many supposed contaminants that damage the purity of the composite A-D information are closed finish funds (CEFs) which personal numerous varieties of bonds (e.g. municipal, excessive grade company, and so forth.). These points commerce on the NYSE simply as if they had been common shares and, as a result of they’re delicate to rates of interest greater than to the general financial system, some analysts look down their noses at them, believing that they’re ruining the general A-D information by their inclusion.

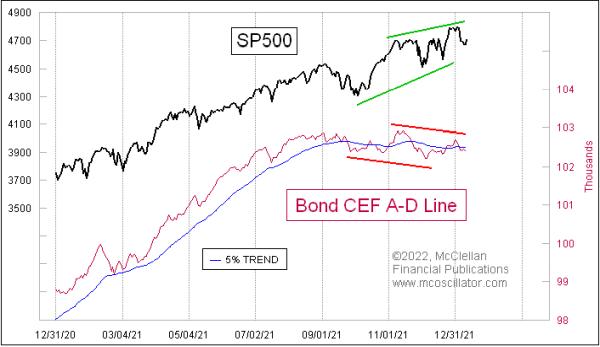

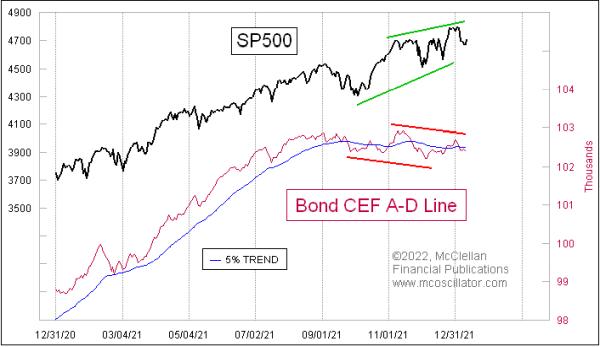

It seems upon examination of the particular information that the bond CEFs really give a very good message concerning the well being of the liquidity stream that impacts your complete inventory market. So, if something, they’re making the composite A-D information higher by advantage of their inclusion in it. This week’s chart exhibits a giant bearish divergence versus the S&P 500.

I possess this information and, so far as I do know, I’m the one analyst who goes to all of this bother, as a result of years in the past I made a decision to check the speculation that these supposed contaminants are ruining the composite A-D information. It took a bunch of labor getting every day information on the entire NYSE shares, determining which of them had been bond CEFs after which calculating advances and declines every day on all of these points. I proceed that work with the assistance of teammates, and infrequently share the insights in our McClellan Market Report and Each day Version.

What I discovered was that the messages from these information are literally actually highly effective and vital. I can now make the argument that the Bond CEF A-D Line may very well be higher than the composite A-D Line, and it’s actually higher than the “common-only” model. See this link for extra concerning the issues with the common-only model.

I spoke about this level years in the past with the late Richard Russell earlier than he died. Russell wrote The Dow Concept Letters for 57 years, proper as much as his dying in 2015. Together with the late Joe Granville, Russell helped to introduce the world to the usage of the NYSE A-D Line in 1962. Earlier than then, virtually no one used it or adopted it, however it turned fashionable that yr as a result of Russell and Granville confirmed their readers that it had made a giant bearish divergence forward of a 27% decline within the DJIA in 1962. Immediately, the concept that you can use the A-D Line to get a warning a couple of dangerous bear market like that was very fashionable.

Russell confided that the identical criticism of the A-D information was provided again within the early Nineteen Sixties, with critics noting that the NYSE had a bunch of utilities and insurance coverage corporations that had been “curiosity delicate”, and which had been presumed to mess up the message of the info. So this criticism of bond CEFs within the trendy A-D information is definitely an previous grievance nonetheless being recycled.

The message of the present divergence proven above is that liquidity has instantly turn out to be an issue and is affecting the extra liquidity-sensitive points first. That may be a prelude to that very same illiquidity coming round and biting the big-cap shares that drive the key averages.

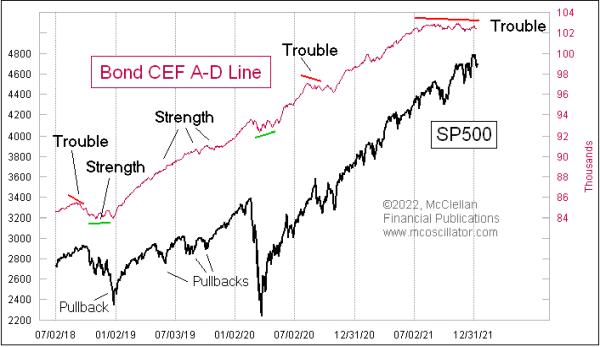

It has been some time since we now have seen a divergence like this one. There was a small one again in August 2020, resulting in only a small quantity of value injury in September 2020. The market rapidly recovered from that one, seen in the midst of this chart:

A whole lot of the time, this A-D Line serves to rebut the message of a value correction by staying sturdy and telling us that no matter issues the inventory market could also be having are usually not liquidity issues. Emotional issues and news-related tales are simpler to recover from extra rapidly than liquidity issues.

There was additionally a small divergence again in September 2018, a warning of bother that unfolded for the S&P 500 in This fall of 2018. By the point that the ultimate value low got here then, the Bond CEF A-D Line was making a bullish divergence, saying that liquidity had been restored, so the inventory market ought to quickly recover from what was bothering it.

These had been very small divergences in comparison with the weak point we’re seeing now. If we go all the best way again to 2007, we will discover one other instance of a giant divergence between the Bond CEF A-D Line and the S&P 500.

The ultimate value excessive then didn’t come till October 2007, however the Bond CEF A-D Line had its peak all the best way again in Might 2007. By the point that the ultimate value excessive got here, this indicator had been screaming about massive illiquidity issues. However few individuals apart from my publication readers knew about that individual message.

Most who hear this message concerning the present divergence between the S&P 500 and the Bond CEF A-D Line will not consider in it, as a result of these bond CEFs are interest-rate delicate contaminants to the correct A-D information. That is really high quality with me that they do not consider in it.

Subscribe to Prime Advisors Nook to be notified every time a brand new publish is added to this weblog!

[ad_2]

Source link

{kind=link}