[ad_1]

Like lots of its friends within the fintech sector, Sofi Applied sciences (SOFI) inventory has been taking a hammering over the previous few months. Nevertheless, that every one modified on Wednesday, after the corporate was granted the long-hoped-for U.S. banking constitution by the Workplace of the Comptroller of the Foreign money.

The much-needed sentiment increase might assist kick off a turnaround and Wedbush’s David Chiaverini believes the ultimate hurdle cleared on the trail to turning into a financial institution ought to “speed up earnings progress.”

Nevertheless, that isn’t the one factor the banking disruptor has going for it. “The corporate is a one-stop store for monetary companies and it is a vital aggressive benefit over neobank rivals who are likely to concentrate on area of interest choices moderately than the total monetary image,” the 5-star analyst mentioned.

SoFi can be well-positioned to compete with legacy shopper finance suppliers as a result of its “streamlined product providing,” whereas a youthful age group are additionally extra more likely to be interested in the corporate moderately than conventional banks, who’re seen as old-fashioned, unfriendly fee-wise, and given their enterprise segments typically “function in silos,” typically have “friction” within the cross-selling course of.

In distinction, SoFi has a aggressive benefit, as a result of its built-in expertise platform Galileo, which supplies a “seamless cross-buying expertise aimed toward a digitally native youthful cohort.”

Furthermore, the corporate has been rising at a quick tempo and is anticipated to proceed doing so. In 4Q21, members crossed the three million threshold, properly above the 1.7 million notched a 12 months in the past and much above the 1 million of two years in the past.

Likewise, income progress has been spectacular; from $600 million final 12 months and $450 million beforehand, the corporate has guided to nearly $1 billion of income in FY2021E.

Whereas SoFi has a five-year plan in place, which Chiaverini thinks is perhaps “overly optimistic” (the income forecast for 2025 is $3.7 billion in comparison with Chiaverini’s $2.9 billion estimate), the analyst nonetheless anticipates a CAGR of 28% over the following 5 years, an “distinctive degree of progress,” which ought to see the corporate attain income of $3.5 billion by 2026.

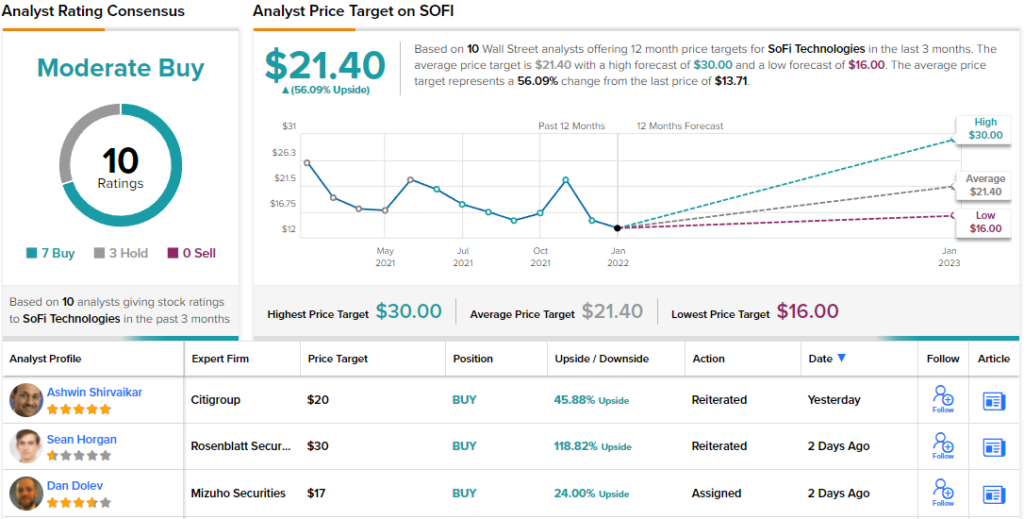

Accordingly, Chiaverini initiated protection on SOFI shares with an Outperform (i.e. Purchase) score and $20 value goal. Traders may very well be pocketing good points of ~46%, ought to the analyst’s forecast hit the mark over the following 12 months. (To observe Chiaverini’s monitor document, click on right here)

Total, SOFI has attracted a complete of 10 analyst critiques lately, together with 7 Buys and three Holds for a Average Purchase consensus score from the Road. SOFI shares are priced at $13.71 and have a median value goal of $21.40, giving the inventory a 56% upside on the one-year timeframe. (See SOFI inventory forecast on TipRanks)

To seek out good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Greatest Shares to Purchase, a newly launched device that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analyst. The content material is meant for use for informational functions solely. It is rather necessary to do your individual evaluation earlier than making any funding.

[ad_2]

Source link