[ad_1]

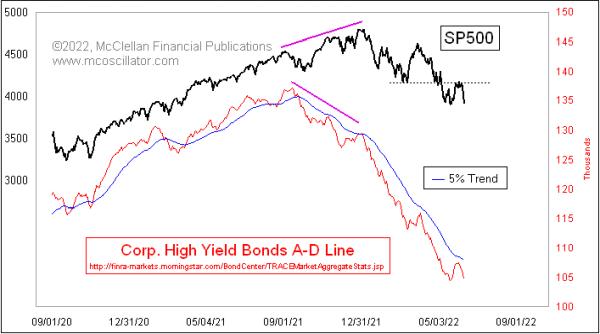

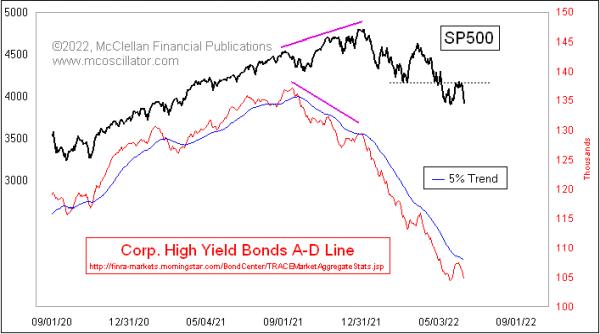

After making an oversold low on Could 19, the S&P 500 had a reasonably spectacular rebound effort, which included 3 actually sturdy breadth days on Could 25-27, 2022. That acquired a variety of analysts speaking a few “breadth thrust” sign of assorted flavors. However the S&P 500 bonked at a resistance degree that had been a previous help degree on the March 2022 lows and, after a number of days, it has now fallen again away from that take a look at of the resistance.

Breadth may need been actually handsome for the NYSE shares in late Could, but it surely was fairly anemic-looking for the inventory market’s fellow vacationers, the high-yield company bonds. This week’s chart contains a each day Advance-Decline Line for these bonds’ A-D information, which is revealed every day by FINRA. These bonds transfer much more just like the inventory market than like T-Bonds. What makes them much more fascinating is that they are usually terribly delicate to liquidity, each good and unhealthy, in order that they operate just like the canaries within the coal mines of Newcastle a few centuries in the past. That’s to say, they inform us when the circumstances are nice for shares and, extra importantly, when liquidity is in brief provide.

This Excessive Yield Bond A-D Line did bounce increased together with the inventory market in late Could 2022, but it surely was a weak bounce that didn’t even make it to the 5% Development line. That’s an exponential transferring common with a 5% smoothing fixed (see this article). The message is that, whereas the bulls had been in a position to mount an honest 3-day bounce, it was achieved with no actual return of sturdy liquidity, which implies that there was not the gasoline for an actual uptrend.

Taking a look at this A-D Line long term, we are able to see that it has proven us divergent prime indications at the entire main tops the place we’d need to have that message.

It additionally instructed us when issues had been trying iffy on the finish of QE1 and QE2, that liquidity actually was not an issue, and the market fairly rapidly acquired over its troubles. The top of QE3 was a unique story, nevertheless, and noticed a extra important decline within the Excessive Yield Bond A-D Line, indicating the liquidity issues that the monetary system was struggling by way of then. After which, in early 2016, this A-D Line shot increased to say that liquidity had by some means been restored.

This A-D Line additionally instructed us concerning the liquidity issues in 2018, when the Fed determined it could do some “quantitative tightening” or QT, shrinking its holdings of T-Bonds and mortgage backed securities (MBS). It confirmed no response when inventory costs rallied in the summertime of 2018, organising the large decline in This fall of that 12 months.

It additionally instructed us concerning the huge liquidity issues we at the moment are dealing with, when it made a divergent prime versus inventory costs in late 2021. We’ve got seen in 2022 what these liquidity issues have meant for the inventory market, and, to this point, this A-D Line isn’t exhibiting us an “all-clear” sign. There may be extra work but for the market to do to dismantle the excesses constructed up throughout QE4.

Subscribe to Prime Advisors Nook to be notified every time a brand new publish is added to this weblog!

[ad_2]

Source link

{kind=link}