[ad_1]

Making the rounds on the monetary blogosphere earlier this month was a Wall Avenue Journal article that detailed millennials’ DIY strategy to investing. Some advisors may be upset to learn tales of younger cash venturing into monetary planning selections with no conventional steerage. Different planners may see this as a possibility.

I am reminded of all of the ink spilled a decade ago about how millennials wouldn’t personal homes like their dad and mom did. Humorous how that narrative died. I imagine millennials may also come round and search assist with their funds as they age. There are a couple of components at play.

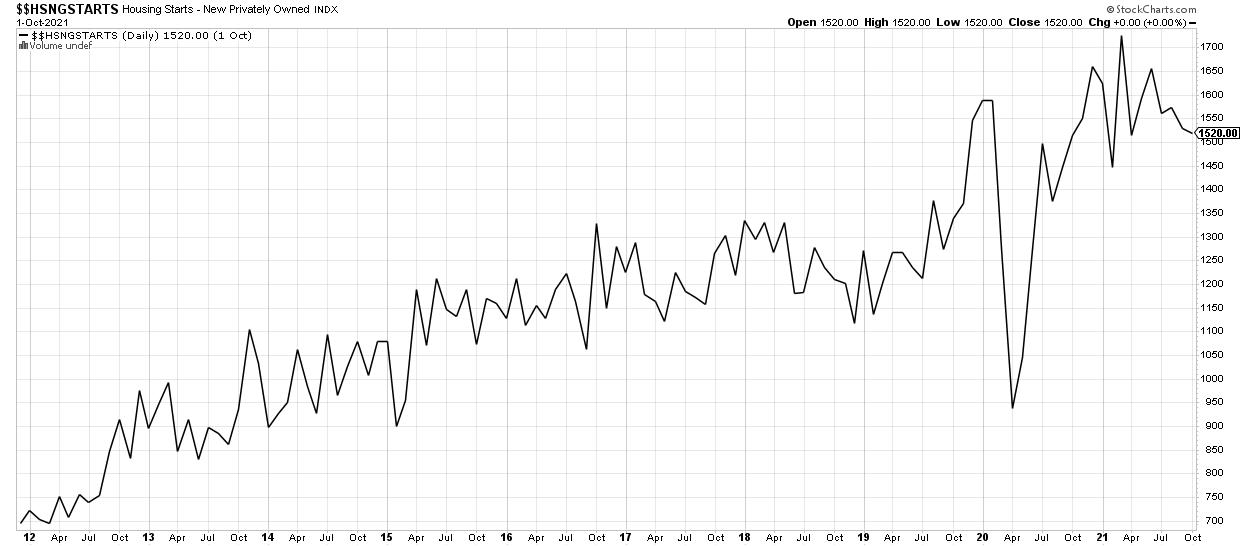

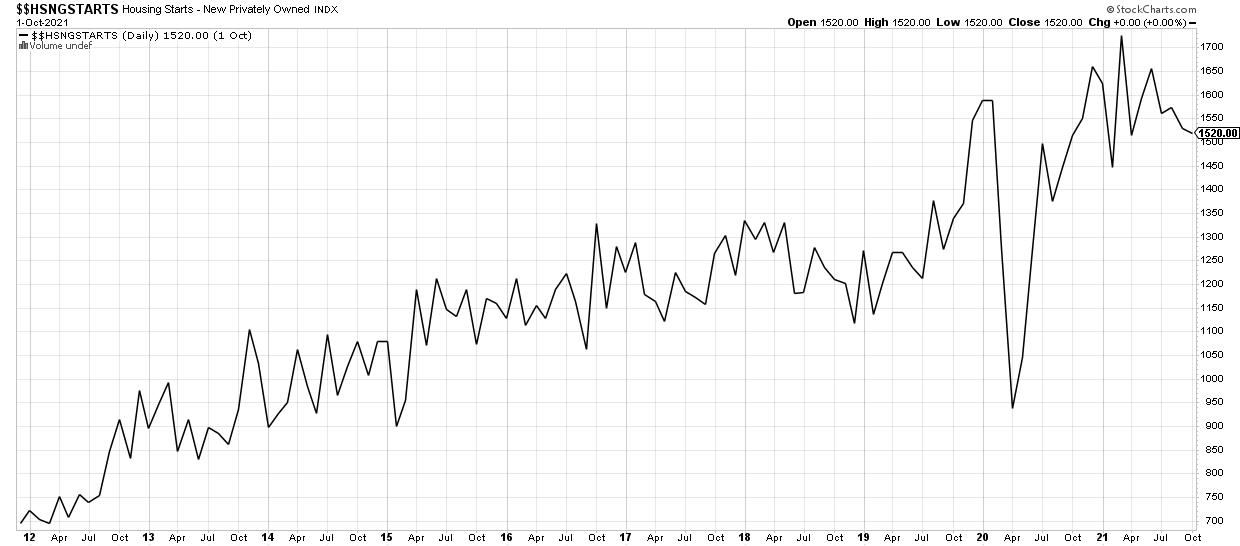

Chart 1: Housing Begins

Chart 1: Housing Begins

For starters, millennials and Gen Z might need only in the near past seen a lift in wealth by way of a booming inventory market, surging cryptocurrencies and thrilling “to the moon” meme shares. Furthermore, a homebuyer from earlier than the pandemic is already sitting on appreciable fairness. Some could have even scored important features from being part of a startup which have seen valuations soar. As time wears on, their portfolios may change into extra of a burden than a supply of thrill.

Chart 2: Case Shiller Residence Value Index

Chart 2: Case Shiller Residence Value Index

Chart 3: Ethereum/USD Relative to SPDR Gold Shares ETF

Chart 3: Ethereum/USD Relative to SPDR Gold Shares ETF

One other factor to think about is that life turns into extra difficult as you become older. There’s not a complete lot of planning required for a younger buck in good well being with a big monetary portfolio. Circumstances change shortly when a partner enters the image, then comes a home, youngsters and caring for getting old dad and mom. That’s the place an skilled monetary advisor can convey enormous worth.

Lastly, time turns into a scarce useful resource by the point somebody hits their late 30s and 40s. Unloading monetary planning duties to knowledgeable opens up extra time to spend with family members somewhat than in entrance of screens and spreadsheets.

Monetary advisors ought to deal with the worth they’ll convey to younger cash. Tax-saving methods, danger administration and easily releasing up a person’s time affords fairly the worth proposition. Serving to these of their 20s and 30s with scholar loans is one other alternative for RIAs.

Current school grads have scholar debt upwards of $30,000, on common, based on the newest information. Monetary planners should be educated on this key space in the event that they need to appeal to the subsequent gen.

How advisors are paid is altering, too. An “belongings below administration” charge association is slowly shifting to an hourly and even flat-fee construction. This development could be useful for younger traders who want primary assist. It can be helpful for these with extra wealth who don’t need to pay 1% per 12 months for basically the identical service (and hours) as a consumer with a lot much less wealth.

Advisors should be capable to talk the talk. A minimum of figuring out the fundamentals of crypto, understanding the attraction of horny (unprofitable) shares, and letting purchasers spend inside cause ought to be the brand new regular if advisors need to attain the subsequent era of wealth.

Mike Zaccardi, CFA, CMT

Funding Author, Zaccardi LLC

Mike Zaccardi is a contract author for monetary advisors and funding corporations. He is a CFA® charterholder and Chartered Market Technician®, and has handed the coursework for the Licensed Monetary Planner program. Mike can also be a finance teacher on the College of North Florida.

Learn More

Subscribe to High Advisors Nook to be notified at any time when a brand new submit is added to this weblog!

[ad_2]

Source link

{kind=link}