[ad_1]

For buyers looking for a transparent path within the markets, some sign that may reduce by means of all of the noise and present simply which shares are prone to acquire regardless of a rising storm of headwinds, the insiders can’t be ignored.

We’re referring to company officers who maintain excessive posts of accountability inside their corporations. They’re CEOs and COOs and CFOs, Exec VPs and members of the Board, and these posts give them two simple attributes. First, a macro-view of the corporate and its prospects; and second, a have to reply to shareholders and Administrators for firm efficiency.

What that boils all the way down to is, company insiders don’t commerce inventory in their very own corporations frivolously. Their strikes are scrutinized from inside – and from the Federal regulators, who require them to publicly report their buying and selling.

Traders can look to those strikes, utilizing TipRanks’ Insiders Scorching Shares instrument. We’ve used that instrument to do exactly that, discover three shares whose insiders have been shopping for just lately. There are different constructive signifiers to comply with; these shares are rated as Robust Buys by the analyst consensus and are projected to choose up steam within the months forward.

Hasbro (HAS)

We’ll begin in a sector that doesn’t at all times get the eye it ought to – kids’s toys. They’ve a prepared and keen buyer base, and the massive toy makers spare no expense on market analysis, or on model acquisition. Hasbro, the primary inventory on our record, is a venerable identify within the trade, going again to 1923, and owns a collection of main toy and recreation names and types, together with Milton Bradley, Kenner, Dungeons & Dragons, My Little Pony, Energy Rangers, Monopoly, Transformers, and PJ Masks. The corporate noticed $6.42 billion on the prime line in 2021, up 17% from the prior yr.

Hasbro is working to enhance its place in regard to its friends by a powerful transfer towards digital and desk gaming. These are development segments of the toy trade, and Hasbro, holding names like D&D and Wizards of the Coast, is well-positioned make beneficial properties right here.

In April of this yr Hasbro reported its 1Q22 outcomes, with the highest line beating the forecast for the fourth quarter in a row whereas the underside line got here in under estimates. On income, the corporate confirmed $1.16 billion, above the $1.14 consensus mark. EPS got here in at 57 cents, lacking the 61-cent forecast.

Regardless of the earnings miss, Hasbro has seen some latest insider purchases which might be pushing the insider sentiment needle into constructive territory. CEO Christian Cocks spent $905,000 on 10,102 shares of Hasbro, whereas Board of Administrators member Michael Raymond Burns made a smaller buy of two,500 shares, paying $219,250.

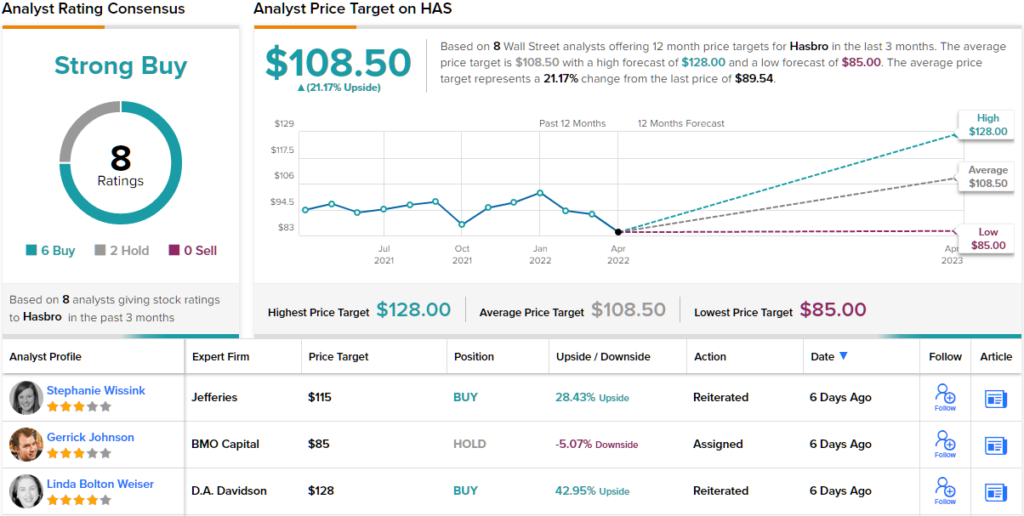

Hasbro has scored followers inside the analyst neighborhood as nicely. Analyst Alok Patel, from Berenberg, charges the inventory a Purchase, whereas his $118 worth goal implies a one-year upside of 32%. (To observe Patel’s monitor document, click on right here)

Backing his stance, the analyst writes: “Our Purchase thesis for HAS is predicted on two key factors. 1) Client merchandise stays resilient; and a pair of) HAS’s first mover benefit in content material pushed methods, coupled with gaming, ought to translate to outperforming friends and the general toys trade… We observe the WoC and Leisure segments continues to develop and permit HAS to higher shield margins in comparison with conventional toy makers. Spectacular development profile of the segments has drawn administration to extend investments in each segments.”

The insiders and Berenberg are bullish right here – and they aren’t outliers. The inventory has 8 latest analyst opinions, with a 6 to 2 breakdown of Buys over Holds supporting its Robust Purchase consensus ranking. The shares are priced at $89.54 and their $108.50 common worth goal suggests an upside of 21% for HAS going ahead. (See HAS inventory forecast on TipRanks)

BlackRock (BLK)

Now we’ll flip to the monetary sector, the place BlackRock, holding greater than $10 trillion in whole AUM, is among the world’s largest asset managers. Since 1988, the corporate has served institutional shoppers, governments, monetary advisors, and high-net-worth people – nevertheless it hasn’t uncared for the small-time retail monetary market, both. BlackRock’s providers can be found in 38 nations and 82 languages, and it’s the firm’s boast that it may possibly tailor a monetary plan for any shopper at any scale.

Earlier this month, BlackRock reported its monetary outcomes for 1Q22, and got here in forward of the estimates. The corporate confirmed a 7% year-over-year acquire on the prime line, with $4.7 billion in whole income. Earnings, at $9.52 per diluted share, grew 18% y/y, and handily beat the $8.74 forecast. In all, it was a powerful begin for 2022.

Clearly, BlackRock’s insiders would agree. William Ford, of the corporate’s Board of Administrators, made two purchases in the course of this month, spending a complete of $2.06 million to purchase 3,000 shares of BLK.

In protection for Morgan Stanley, analyst Michael Cyprys seems to echo the Director’s bullish sentiment. He writes, “BLK stays targeted on investing for development whereas staying prudent ought to market situations grow to be extra challenged. However we’re assured in BLK’s monitor document to ship return on spend by way of sturdy topline development alternatives…”

“We view BLK as an all-weather identify among the many conventional asset mgrs given their diversified/scale enterprise mannequin that may higher navigate a harder macro backdrop, harness Aladdin expertise capabilities to unlock development, and act strategically from a place of energy,” the analyst added.

These feedback again up Cyprys’ Obese (i.e. Purchase) ranking on this monetary inventory, whereas his worth goal, at $932, signifies confidence in ~40% upside by yr’s finish. (To observe Cyprys’ monitor document, click on right here)

Main monetary corporations sometimes get loads of consideration from the Road, and BlackRock is not any exception. There are 14 latest analyst opinions right here, and so they embrace 11 to Purchase in opposition to 3 to Maintain for a Robust Purchase consensus. BLK is promoting for $668.28 and its $870.07 common worth goal implies ~30% upside within the coming months. (See BLK inventory forecast on TipRanks)

Inozyme Pharma (INZY)

Let’s wrap up with a biopharmaceutical agency. Inozyme is researching new therapies for uncommon ailments of the vascular and skeletal methods, in addition to smooth tissue ailments. Particularly, the corporate is specializing in a category of harmful situations with few therapies: irregular mineralization problems, which result in everlasting and crippling sicknesses. The corporate’s scientific program is engaged on new therapeutics to deal with genetic deficiencies within the ENPP1 and ABCC6 genes.

Inozyme’s analysis is at the moment narrowed in a single drug candidate, INZ-701, which is taken into account significantly promising for a variety of functions. The corporate has two Section 1/2 trials underway, testing the drug in opposition to each ENPP1 and ABCC6 deficiencies. Earlier this month, Inozyme hit a serious milestone when it introduced constructive preliminary knowledge from each trials.

On April 4, Inozyme launched early outcomes displaying that the lowest-dose cohort within the ENPP1 examine delivered a sustained enchancment in plasma pyrophosphate ranges. Whereas this was based mostly on solely 3 sufferers, all confirmed ranges that evaluate to observations of wholesome people. Moreover, all three sufferers tolerated the drug nicely, with few unwanted effects. Inozyme is continuing with dosing the second examine cohort on the subsequent dose stage. Topline knowledge on this examine is anticipated in 2H22.

Subsequent, on April 12, the corporate introduced that it had dosed the primary affected person in its examine of ABCC6 deficiency. That is one other Section 1/2 scientific trial that may check dose escalation and toleration, together with preliminary biomarker and security knowledge. The corporate expects to launch this info in 2Q22. Collectively, these bulletins have been a serious even for the corporate, as they mark an necessary de-risking of INZ-701.

Medical trials value cash, nonetheless, and Inozyme has additionally introduced, on April 14, an providing of greater than 16 million shares of inventory at $3.69 per share. An insider, Robert Hopfner of the Board of Administrators, purchased in large through the sale, selecting up 1,070,000 shares for a complete worth of almost $3.95 million.

A transparent description of the bullish view on Inozyme comes from Christopher Raymond, of Piper Sandler, who says, “We advocate buyers take an in depth take a look at this identify as we consider this inventory serves as a main instance of ‘throwing the infant out with the bathwater’ within the midst of one in all biotech’s deepest and most extended swoons. Simply by wanting on the chart, one would assume a serious failure or pipeline reset has taken place. On the contrary, nonetheless, ‘701 had preliminary PoC knowledge that unlocks a $0.5B WW income alternative for a severe ultra-orphan illness (ENPP1 deficiency) with no significant scientific alternate options. Coupling this with a significant alternative in one other ultra-orphan illness (ABCC6 deficiency), with PoC coming quickly, we expect this identify has a threat/reward that requires a better look.”

Consistent with these bullish feedback, Raymond offers INZY shares an Obese (i.e. Purchase) ranking, and his $40 worth goal implies a strong 681% one-year upside potential. (To observe Raymond’s monitor document, click on right here)

Neither the insider nor the Piper Sandler analyst are outliers right here, as Wall Road offers INZY shares a unanimous Robust Purchase, based mostly 5 constructive analyst opinions. The inventory has a mean goal of $30, which suggests ~486% upside from the present buying and selling worth of $5.12. (See INZY inventory forecast on TipRanks)

To search out good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Greatest Shares to Purchase, a newly launched instrument that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is rather necessary to do your individual evaluation earlier than making any funding.

[ad_2]

Source link